Do any mutual funds reliably generate significant alpha and, if so, do fund investors receive this alpha? In their June 2015 paper entitled “Active Managers Are Skilled”, Jonathan Berk and Jules Van Binsbergen examine interactions among equity mutual fund gross alpha, assets under management, fees and net alpha. To measure a practical gross alpha, they benchmark active mutual fund gross performance against an historical best-fit linear combination of net returns from contemporaneously available Vanguard funds. To account for the effects of mutual fund size, they measure monthly dollar value added by the fund manager as gross alpha times assets under management. This approach accounts for competition among funds, whereby investors chase an outperforming fund until its alpha drops to zero. They then estimate fund manager skill as average monthly valued added divided by the standard error of the monthly value added series. Using gross monthly returns and fees for a broad survivorship bias-free sample of of active equity mutual funds and net monthly returns for Vanguard mutual funds during January 1977 through March 2011, they find that:

- Most active equity funds destroy value, but most of the capital is controlled by managers who add value. Specifically:

- The average (median) monthly value added per fund is +$270,000 (-$20,000) in year 2000 dollars.

- Only 43% of funds have positive average value added.

- The tenth (decile) of fund managers with the highest past skill control roughly one quarter of total active mutual fund capital.

- Differences in fund manager skill persist for as long as 10 years.

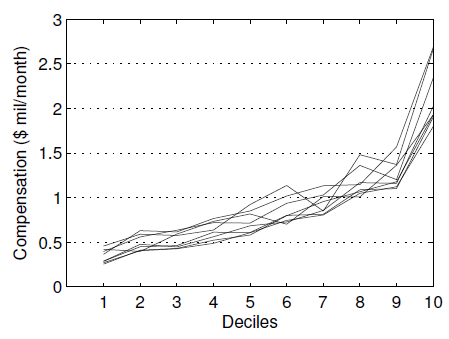

- Fund manager compensation (fee in dollars) relates positively to fund manager skill (see the chart below). In fact, compensation is a better predictor of fund value added than is the specified measure of skill.

- The average net alpha of sampled funds is not significantly different from zero. In other words, fund managers do not share the benefits of their skill with fund investors.

- Restricting the sample to funds that invest only in U.S. stocks results in a significantly negative overall net alpha, suggesting that the most skilled managers gravitate toward less competitive international equity markets.

The following chart, taken from the paper, relates future average monthly fund manager compensation (vertical axix) to current exhibited skill decile (horizontal axis). Each line represents a different future horizon ranging from three to 10 years . Results indicate that future compensation relates systematically and persistently to proven skill level.

This relationship ultimately translates to fund managers (not investors) keeping the benefits of persistence in fund value added.

In summary, evidence from competitively dynamic estimates of skill among mutual fund managers indicates that persistent outperformance exists and that the market rewards it, but value added accrues on average to fund managers and not to fund investors.

Cautions regarding findings include:

- Ancillary findings suggest exploitation of non-U.S. markets is important to fund performance, but the authors do not explore whether degree of international diversification reliably relates to degree of outperformance. Investors may want to focus on fund managers that are relatively concentrated in non-U.S. stocks.

- The study does not address trend in overall industry outperformance over time and does not include data for recent years.